The Two Things’ Politicians Hide About Our Social Security

Economizer Red Zone Edition #51526

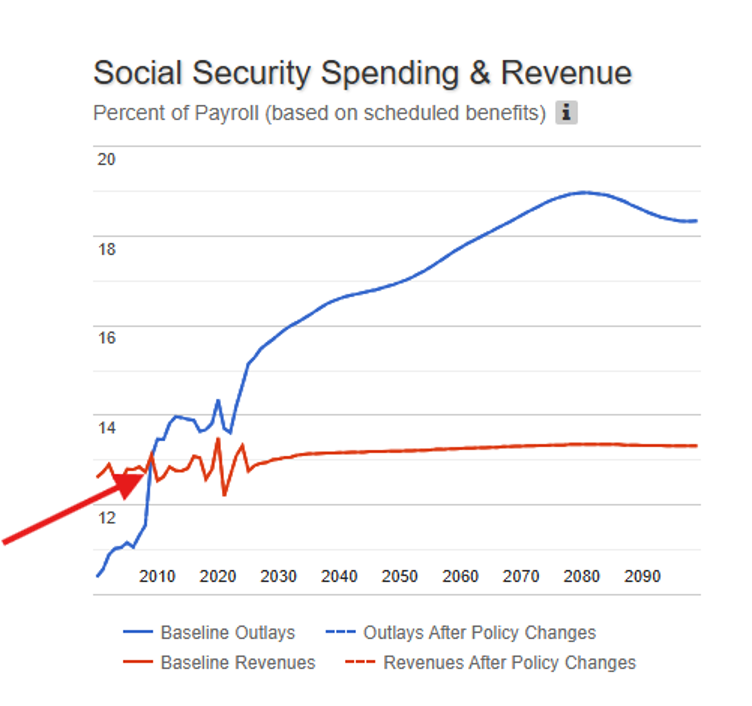

#1 The trust fund will run out of money- Guaranteed.

We knew about this 26 years ago because the money coming in was less than benefits being paid.

out 2010 (see red arrow). This isn’t new folks!

#2 Benefits for everyone will be cut close to 25% when the trust fund runs out for everyone. Even for people that have been collecting for years.

A short statement for the conspiracy theorists who assume the Congress stole and spent the trust fund money.

The congress stole it stems from a misunderstanding of how the Social Security program is financed. Here is what really happens:

Every dollar of Social Security (FICA) tax collections is immediately converted into U.S. Treasury notes.

The government spends our money to fund government operations.

The Treasury notes held by the Social Security system are paid interest.

You must remember that our tax dollars just don’t sit in a shoe box- it is earning interest!

Short History Lesson

The Very Near-Insolvency of the Trust Fund happened in the Early 1980.

In the early 1980s, a solvency crisis involved the trust fund. The 1982 Social Security Trustees Report projected that in the absence of legislative changes, the trust fund would become insolvent by July 1983. To build up the trust fund temporarily, (talk about waiting until the last minute). Congress permitted the Social Security fund to borrow from the DI (Disability Income) and HI (Hospital Insurance) trust funds through the end of 1982.

On November 5, 1982, the balance of the SS trust fund had fallen to zero, and continuing tax revenues were insufficient to pay in full the benefit checks that were delivered on November 3. (Some of the old-timers may remember the term Rubber Check). To cover the shortfall, the Secretary of the Treasury authorized a $581 million loan from the DI trust fund to the OASI trust fund. Additional loans from the DI and HI trust funds to the S.S. trust fund were made as well. FYI the loans were paid back with interest.

Ideas to fix the problem of a soon to be bankrupt trust fund.

One big measure is Raising the Cap on Taxable Income. Because many people think that the rich should pay more into Social Security!

This has some serious drawbacks. Which they keep quietly hidden.

The more you pay into the system, the more you are going to get out of the system.

Raising the cap on taxable income has a serious downside.

Since the Social Security program began in 1935, the law has set a limit on the amount of earnings subject to Social Security tax. In 1935, the wage base was $3,000. It has gradually increased over the years. For many years now, that increase has been automatic based on growth in the national average wage index. The current (2026) wage base is $184,500.

What that means is many wealth American’s Like Buffet, Amazon and Facebook (Meta) founders pay the same amount as many others who make $184,500 annually. Example, anyone who makes more than $184,500 per year pays the same amount in Social Security taxes even if their income exceeds $200,000, $1 million, or even $1 billion a year, they all pay the same Social Security taxes.

Under our SS program, Social Security benefit payments are directly tied to the amount of earnings on which you pay Social Security taxes. Simply put: The more you pay into the system, the more you are going to get out of the system.

In other words, if rich people paid taxes on their very high incomes, they are going to eventually get Social Security benefits based on those same very high incomes. What that means is that much of the extra income from the higher taxes that they pay will be offset by the extra Social Security benefits they will receive someday. (Makes sense right). I often state that in mathematics if you change one side of the equation then the other side changes as well.

To stop that from happening, and to make this popular reform (Tax the Rich) proposal work, what you would probably have to do is greatly increase the taxable wage base, and at the same time set a limit on the amount of benefits payable.

In other words, we’d be telling rich people this: “You are going to pay a lot more in Social Security taxes, but you’re not going to get very much more in Social Security benefits. I am sure that will go over Big!

Some options that may help but are not the full solution to avoid the benefits cuts:

Raise the Retirement Age to 70 by 2060.

Downside: working till age 70 might be tough. And a side issue employers will face higher health care costs for older workers.

Reduce Cost-of-Living Adjustments (COLAs) paid to Social Security Beneficiaries using the Chained CPI. (Which sucks)

Downside: COLA reductions are cumulative. The longer you live, the more you will suffer financially.

Reduce Benefits by 5 percent for All Future Retirees.

Downside: many lower-income beneficiaries could not afford the reduction.

Means Test the Program, Lowering Benefits to Wealthy People who save diligently

Downside: Ensures that Social Security is paid only to those who need it most and would turn Social Security into a welfare program.

Raise Social Security Payroll Tax by 1 or 2 Percent for both the employer and employee

Downside: An extra tax burden would cripple savings, especially contributions to 401(k) and employer matches.

Income Tax on 100% of Social Security Benefits (currently, a max of 85% is taxed)

Downside: higher taxes for everyone.

Steps to take:

Write to our Washington legislators.

Start saving a Social Security Reduction emergency fund.

Begin to budget more aggressively.

Take action so you are not blindsided.

Reduce costs on your investments.

Steps to do today:

Don’t miss next week’s issue.

Interesting!